You never want to imagine anything happening to your child, but what if the baby gets sick? It’s hard to think about getting insurance for children. A child’s insurability can change quickly and unexpectedly and having life insurance for your child can guarantee a lifetime of worry-free coverage. Having a new baby adds new expenses, but life insurance doesn’t need to be costly. Here’s everything you need to know about getting life insurance for children in Canada.

Does a child need life insurance?

No one wants to talk about getting life insurance for children, as it means considering the unthinkable. Heck, parents are busy enough trying to get their child to sleep or stop crying, so they may not even consider it.

Life is unpredictable, and an insurance policy for your new baby or young child could make life a lot easier should the unthinkable occur. Many families with sick children take time off work and incur major financial losses. Life insurance can’t replace loved ones, but it could help you carry on.

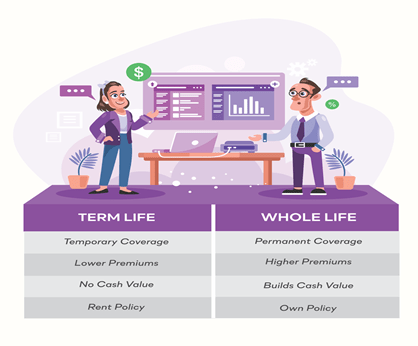

Most child life policies don’t require an exam, and parents or grandparents can purchase the coverage on children and grandchildren. Whole life policies are very straightforward.

Consider three strategic reasons why insuring your kids early is good parenting:

- The money that builds up in your children’s policies can fund their advanced education later. Universal life is a good variable option with an investment component that builds a tax-exempt cash value.

- Give your children long-term financial stability to fund forthcoming expensive life events. Start contributing to a large whole-life policy when your kids are little. Cashing out as adults decades later can enable them to buy homes or establish for their own families.

- If they become ill as kids or adults, they won’t have to worry about being uninsurable. Thanks to you, they’ll have lifelong security already. Otherwise, they would be unable to leave life insurance death benefits to their dependents.