Life insurance is viewed as a financial safety net and is essential for anyone who has people depending on them. These could be children who are going to school, sick parents, or a family that needs their day-to-day bills covered. In case of premature death, the resulting loss of income may have an adverse effect on the lives of the surviving family members. The goal of life insurance is often to supplement the missing income and allow your dependents to maintain their lifestyle.

If you have family property secured as collateral for a loan (a fancy way of saying mortgage 😉, it can be an excellent idea to have life insurance that can cover the entirety of this debt. If you pass away, the loan and required payments do not just magically disappear. If the surviving family members cannot make the payments, they may be evicted or forced to sell, leaving them homeless. The same principle applies if you co-signed your children’s student loan, they are left with the burden of paying the whole amount on their own in case you pass away

In most families, it is the breadwinner that sees the need to own life insurance. However, it is worth mentioning that even the spouse who stays at home should consider getting life insurance. While they may not bring in money to the household, they have roles and responsibilities that allow the family to save on expenses such as daycare. If they were to pass away, someone would have to assume the role. This would result in a lower income if the working spouse were forced to either stay at home or to pay for a caregiver. It is, therefore, a good idea to have life insurance for both spouses.

No te pierdas esta gran platica… Si estas pensando en comprar casa y obtener el mejor seguro hipotecario, estaremos en vivo 6:30 pm visita mi pagina y sigueme para que puedas conectarte directo el viernes 27 de mayo. 647 823 1053 #linethorea

Protect yourself against the emergency medical costs of unexpected accident or sickness while in Canada. One day in hospital can cost as much as $5,000!

For visitors, landed immigrants, returning Canadians and work/student visas.

We specialize in parent, grandparent super visa insurance and were the first company in Canada to offer a convenient monthly payment option. A two year policy is also available.

Enhanced Plan

Comprehensive emergency medical benefit plan.

Includes coverage for stable pre-existing medical conditions*.

Available up to age 85.

Coverage limits from $15,000 to $200,000.

Wide range of deductibles from $0 to $10,000.

Deductibles apply per person per policy.

Companion and family rates available.

Monthly Payment Option and upgrade to 2-year term available.

$25,000 Accidental Death and Dismemberment included.

Dental Accident (up to $4,000) and Relief of Dental Pain (up to $300).

$50,000 Extra Injury coverage included with the $100,000 option.

Continuing Treatment Provision with no specific limit on the number of follow-up visits.

Unique 90-Day Provision which reinstates benefits that might be cut off after an emergency ends.

Standard Plan

Comprehensive emergency medical benefit plan.

Excludes coverage for pre-existing medical conditions.

Available for ages 55 to 85.

Coverage limits from $15,000 to $200,000.

Wide range of deductibles from $0 to $10,000.

Deductibles apply per person per policy.

Companion rates available.

Monthly Payment Option and upgrade to 2-year term available.

$25,000 Accidental Death and Dismemberment included.

Dental Accident (up to $4,000) and Relief of Dental Pain (up to $300).

$50,000 Extra Injury coverage included with the $100,000 option.

Continuing Treatment Provision with no specific limit on the number of follow-up visits.

Unique 90-Day Provision which reinstates benefits that might be cut off after an emergency ends.

Basic Plan

Reduced benefit emergency medical plan.

Excludes coverage for pre-existing medical conditions.

Available for all ages.

Coverage limits from $15,000 to $200,000.

Wide range of deductibles from $0 to $10,000.

Deductibles apply per person per claim.

Companion and family rates available.

Monthly Payment Option and upgrade to 2-year term available.

If you’re buying a home or renewing an existing mortgage, you may be offered group insurance by your lender or broker. You put a lot of money towards your home, so it’s worth taking steps now to protect your investment. Mortgage insurance is typically marketed towards new homeowners who may be concerned that an unexpected death or illness could leave their loved ones with a large mortgage. Personal life insurance like mortgage insurance can perform a similar function for you but isn’t tied to just covering your mortgage. It’s designed to provide your beneficiaries with money in the event of your death. Its flexibility allows your beneficiaries to use the money for whatever purpose they wish. It’s an individual insurance product. Main differences Mortgage insurance from the bank covers the balance of your mortgage, which decreases as the mortgage is paid down. Personal mortgage life insurance coverage, meanwhile, stays the same and isn’t linked to your mortgage. The insurance from the bank doesn’t protect you. Instead, it protects your lender Mortgage insurance from the bank ends when your home is paid off. A personal life insurance policy is unaffected by your mortgage ending and can keep providing you and your family with protection in the years that follow. Mortgage insurance from the bank provided through a financial institution is typically quick and easy to arrange, and usually only requires answering a few health-related questions. Buying personal life insurance, on the other hand, typically takes longer and involves delving into your medical history. The bank is considered your benefactor, not your family. While the mortgage will be paid off, your family won’t receive anything. Also, the amount of coverage declines as you pay down your mortgage. With regular life insurance, your coverage remains the same. And if you decide to change lenders, your insurance isn’t portable, so you’ll lose your coverage.

Protect yourself against the emergency medical costs of unexpected accident or sickness while in Canada. One day in hospital can cost as much as $5,000! For visitors, landed immigrants, returning Canadians and work/student visas, super visa any status in Ontario can get protected with this medical plan. Lineth Orea Aguirre Life, Health and travel Insurance Advisor 647 823 1053

A vacation is really an investment in your happiness. And when that vacation starts off with a canceled flight, a missed connection, a missing bag or another travel hiccup, that happy travel feeling fades. Travel insurance can help make these situations better. After saving for a while, you’ve just paid $3,000 for your long-awaited trip to Iceland. Whew! You know you should probably buy travel insurance, too, but your finger hesitates over the “buy now” button. “Is travel insurance really worth it?” you wonder. “I could spend that money on a nice dinner in Reykjavik instead… Why should I buy travel insurance? What does it even do for me?” We’re so glad you asked. 1. Because medical emergencies often happen while traveling. 2. Because it can be really expensive to get emergency medical care overseas. 3. Because you can’t risk losing money on an emergency trip cancellation. 4. Because cruise lines really hate giving refunds. 5.Because delayed and cancelled flights are common. 6.Because peace of mind is priceless. Whether you’re planning a solo adventure or a grand, multi-generational getaway, the whole point is to relax and enjoy the journey. Travel insurance can ease your anxiety because you know you have protection in case of common travel mishaps. Not only that, but you know you’re never alone. Remember You can buy travel insurance if you are going to travel between Canada and outside Canada. Another important thing If you are going to received family, friends, parents you also can have an emergency medical plan.

You never want to imagine anything happening to your child, but what if the baby gets sick? It’s hard to think about getting insurance for children. A child’s insurability can change quickly and unexpectedly and having life insurance for your child can guarantee a lifetime of worry-free coverage. Having a new baby adds new expenses, but life insurance doesn’t need to be costly. Here’s everything you need to know about getting life insurance for children in Canada.

Does a child need life insurance?

No one wants to talk about getting life insurance for children, as it means considering the unthinkable. Heck, parents are busy enough trying to get their child to sleep or stop crying, so they may not even consider it.

Life is unpredictable, and an insurance policy for your new baby or young child could make life a lot easier should the unthinkable occur. Many families with sick children take time off work and incur major financial losses. Life insurance can’t replace loved ones, but it could help you carry on.

Most child life policies don’t require an exam, and parents or grandparents can purchase the coverage on children and grandchildren. Whole life policies are very straightforward.

Consider three strategic reasons why insuring your kids early is good parenting:

The money that builds up in your children’s policies can fund their advanced education later. Universal life is a good variable option with an investment component that builds a tax-exempt cash value.

Give your children long-term financial stability to fund forthcoming expensive life events. Start contributing to a large whole-life policy when your kids are little. Cashing out as adults decades later can enable them to buy homes or establish for their own families.

If they become ill as kids or adults, they won’t have to worry about being uninsurable. Thanks to you, they’ll have lifelong security already. Otherwise, they would be unable to leave life insurance death benefits to their dependents.

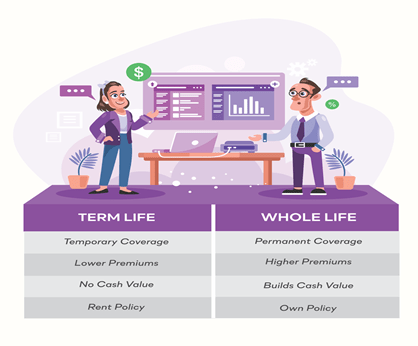

Term life policies are typically more affordable than permanent policies because term life coverage is temporary and does not accrue cash value. Term policies may be a good fit for parents or for spouses who want to ensure the financial security of their dependents during a critical time in their life, such as paying a mortgage or paying for a child’s education.

Permanent Life Permanent life insurance provides lifetime coverage (as long as you pay your premiums on time) and includes a cash value component that is not offered by term life policies. You can borrow against the cash value of the policy or collect it when the policy is surrendered. A permanent policy may be a good fit for someone who wants lifetime coverage and is interested in the investment vehicle it offers.

First thing first: If you or someone you know is considering suicide, please talk to someone about your thoughts. The suicide provision states that, if you die within two years after buying the #policy as a result of suicide, the carrier will contest your claim and will not pay your beneficiaries. After two years, an insurer can’t challenge the death claim and must pay the #benefit.

Life insurance is one of those things that just about everyone needs but far too few people have. It’s easy to put off purchasing a policy when you’re young and relatively healthy. But the longer you wait, the greater the chances of something happening before you get yourself coverage. Maybe buying life insurance been on your to-do list for a while but you haven’t gotten around to it yet. Check out these 10 reasons why you can’t afford to wait any longer.

1. Replace Lost Income

Life insurance works to provide financial security to your loved ones after you pass away. You must consider what would happen if you were to die suddenly. This is especially true if your loved ones rely solely on your income. Get yourself adequate coverage. That way, you won’t leave your loved ones helpless when the monthly bills come around.

2. Cover Burial Expenses

Sadly, even a basic funeral service can run upwards of several thousand dollars. While it’s possible to prepay for your funeral, people don’t often think that far ahead. Pre-payment can ensure everything is in place for your loved ones after you die. However, there are risks to pre-payment. Life insurance can give you and your beneficiaries more of a guarantee, lifting a burden off them as well as yourself.

3. Pay Off Debt

Just because you die doesn’t necessarily mean your debts will disappear. In the instance that you and your spouse have co-signed for a mortgage or other loans, your spouse may become entirely responsible for repayment. The other outcome could result in creditors trying to collect from your estate. While that gets rid of your debts, your heirs will receive the depleted remainder. Life insurance allows those you leave behind to take care of any lingering financial responsibilities.

4. College Planning

There are several ways to save money for your child’s education. You may not have thought that a life insurance could be a option. But insurance payouts can provide a good supplement your savings. If your child ends up borrowing money to get through school, the insurance proceeds could also help wipe out pesky student loans.

5. Build Cash Value

Term Life Insurance is a type of life insurance, stays in place for a set period. But another option, whole life insurance, provides permanent coverage that only ends if you cancel the policy. Whole Life Insurance allows you to build up cash value over time, an attractive prospect to any people. That cash value acts as an extra cushion that you can tap at any time. This may come in handy if you have a financial emergency down the road.

6. Diversify Investments

Some people also use life insurance as an investment tool with universal life polices. These policies are tied to a specific investment product. Then policyholders receive dividend payments based on the product’s performance. Before you dive into this type of insurance, you’ll want to read the fine print. That way you’ll know the potential risks and returns before you commit.

7. Business Planning

If you own a business, it’s vital that you have life insurance. This covers your obligations, so your hard work doesn’t go to waste. Are you involved in a partnership with someone else? You should both have coverage. That way, if one of you dies, the other isn’t left holding the heavy financial bag.

8. Estate Taxes

When someone passes away, their heirs often face estate and inheritance taxes on any assets they receive. If you’re worried about your loved ones getting hit with a big tax bill, a life insurance policy can help cover these added costs.

9. Coverage is Affordable

One of the excuses people tend to make for not buying life insurance is the cost. But truthfully, coverage often ends up affordable for most people. Term life tends to be less expensive than whole or universal life. Plus, the younger and healthier you are, the lower your premiums will be. Unless you smoke or have a pre-existing health condition, you could find coverage for as little as $1 a day.

10. Peace of Mind

No one can truly predict the future. But having life insurance means you and your loved ones can prepare for any eventuality. Even with a small policy, you may find yourself sleeping a little easier at night knowing that your family has protection in place should something happen to you.

{kind=link}